A few simple steps can make a big difference in making your money work harder for you.

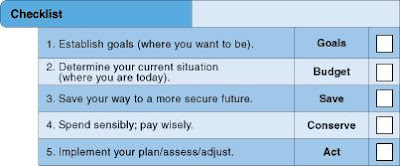

ESTABLISH GOALS – WHERE DO YOU WANT TO BE?

Use the work sheets directly below to help you identify your goals. Print them and fill them in.

Without goals, it is difficult to accomplish anything. When you think about your future and what you want to achieve, it is helpful to establish a timeframe.

- Short-term: such as paying off credit card debt, saving for a vacation or buying new clothes.

- Intermediate: such as saving to buy a car.

- Long-term: such as saving for education or for retirement.

Estimate the cost of each goal and the date you want to achieve it. Then figure out how much you need to save each month. Try to set realistic goals and saving requirements.

CREATE A BUDGET. DETERMINE YOUR CURRENT SITUATION. WHERE ARE YOU TODAY?

Now that you have figured out your financial goals, you are ready to create a budget that will help you attain them. Print the budget work sheets below and write in your budget figures. Start by writing down your expenses (under Current Monthly Expenses).

MONTHLY FIXED EXPENSES – start with monthly fixed expenses such as regular savings, housing, groceries, utilities, and car payments. Put these continuing obligations under the heading: Fixed.

Use checking account statements, credit card statements, receipts and other records to help you complete this estimate. Be realistic - it is better to estimate high than low.

Remember that savings is considered an expense even though you keep the money. You work hard. You deserve to keep some of what you earn every month. Savings is the key to meeting your financial goals.

Make estimates for all money spent - regardless of how you pay: cash, check, credit card, debit card, automatic checking account withdrawals or savings through work plans such as retirement packages.

MONTHLY VARIABLE EXPENSES – once you have noted all your fixed expenses, write down your expenses that vary each month such as clothing, vacations, gifts and personal spending money. Put these expenses under the heading: Variable. You might have these expenses every month, but the amount you spend could change.

Get a handle on variable expenses by writing down every expense for a month - even small purchases. Use a small notebook or other informal method to track your spending. This is very important because it is the best way to understand your current spending behavior. Get receipts for all purchases - especially those you make with cash. Record and categorize each transaction. You may be surprised at how much you spend in certain categories.

Use a notebook to write down every purchase you make for one month. This is the best way to understand your current spending behavior.

List your monthly income

Now that you have figured out your expenses, write down your monthly income after all taxes and deductions. Write this under the heading: Monthly Income. Make sure this figure reflects the total take-home pay for your household after all taxes and deductions.

NOW COMPARE EXPENSES TO INCOME – one of the advantages of doing a comparison of expenses to income is that it provides a quick reality check. If you are spending more than you are bringing home every month in income, you have a deficit. If you are spending less than you are bringing home, you have a surplus. In either case, it is time to step back and consider some options.

If you have a deficit: Spending more than you are bringing home, ask yourself:

- Can I spend less in some of my variable expenses?

- How much interest am I paying with credit card and other loans?

- Where did my money go? (Consider writing down everything you spend for a month.

If you have a surplus: Spending less than you are bringing home, ask yourself:

- Am I saving enough to meet my goals?

- Are my spending estimates accurate?

- Have I included all my fixed and variable expenses?

SAVE YOUR WAY TO A MORE SECURE FUTURE

An estimated seventy-five percent of families will experience a major financial setback in any given ten-year period. The economy and the job market are good now, but that could change. It is smart to be prepared for financial thunderstorms.

SAVE EARLY, SAVE OFTEN – a consistent, long-term saving program can help you achieve your goals. It also can help you build a financial safety net. Experts recommend that you save from three to six months worth of living expenses for emergencies.

Savings grow beyond what you contribute because of compound interest. Over time, the value of compound interest works to every saver's advantage.

For example, if you save $75 a month for five years and earn five-percent interest, the $4,500 you contributed would grow to $5,122 because of the compounding interest.

It is easy to figure out how long it will take you to double the money you save. It's called the Rule of 72. You take the interest you are earning on your money and divide that number into 72. The result is roughly the number of years it will take your principal to double.

For example, if you are earning 5 percent on your money, you divide 72 by 5 and you get 14.4. Your principal will double in 14.4 years without further contributions.

Keep in mind, however, that inflation reduces the return on your money.

For example, five percent-interest, adjusted for three-percent inflation, only nets a two-percent real return.

WHAT YOU DON’T SEE, YOU DON’T SPEND – saving means giving up something now, so you will have more in the future. It is not easy deferring or eliminating purchasing things you want today.

It helps to pay yourself first. Take a portion of savings from every paycheck before you pay any bills. Use your company's payroll deduction plan if available. Arrange for a fixed amount to be taken out so that you never see it. What you do not see, you do not spend. You also can direct automatic checking account withdrawals into a savings account or money market.

Join the company's retirement-savings plan. Your contribution avoids current taxes and accumulates tax deferred. In addition, companies sometimes match some of your contributions.

For example, for every dollar you contribute, the company could contribute 25 cents. That would be a 25-percent return on your money.

OTHER SAVING TIPS:

- When you get a raise, save all or most of it.

- Pay off your credit card balances and save the money you're no longer spending on interest.

- Shift credit card balances to a card with a lower interest rate and use the savings to pay off the balance.

- Keep your car a year or two longer. Do routine maintenance and make regular repairs.

- Save the money you would have spent on a new car.

- Stop smoking.

- Take $5 from your wallet everyday and put it in a safe place. That will add up to $1,825 in a year.

- Shop with a list and stick to it.

- Don't buy any new clothes until you've paid off your current wardrobe.

- Eat more meals at home.

- Look for inexpensive entertainment: zoos, museums, parks, walks, biking, library books, concerts, movies and picnics.

- Shop for less expensive insurance.

- Drop subscriptions to publications you don't read.

- Postpone purchases or consider fewer features on the items you plan to purchase.

The less you spend, the more you can save. Moreover, the longer you can consistently save, the faster your savings will grow.

CONSERVE – SPEND SENSIBLY/PAY WISELY

Experts recommend paying with cash whenever possible. This helps you spend less than you otherwise would have spent if you had charged the purchase. You will also avoid credit card interest charges and check-cashing fees.

APPLYING FOR A CREDIT CARD – when you choose to apply for a credit card, shop carefully. There is a wide range of annual fees, interest rates, grace periods for which you do not pay interest, late fee charges, cash advance charges and other fees. Watch out for "teaser" rates that offer low rates initially but increase dramatically soon after.

To get a card with a low interest rate, you will first need to pay down your current debt. Second, let a year go by without applying for any new cards or loans, or accepting a higher credit limit on your current cards. Third, cancel cards you are not currently using. As a rule, limit yourself to two credit cards. Fourth, get a copy of your credit report and check it for accuracy.

CREDIT CARDS – Visa, MasterCard, and Discover are revolving-credit cards. You can charge up to a certain limit and carry most of the balance forward from month to month. Be careful about only paying the minimum amount due. This is a very expensive form of credit because of interest charges. The best rule is to charge only what you can afford to pay off in full every month. Then actually pay the entire balance when you get the bill.

When you are paying down credit card debt, start with the card with the highest interest rate. Pay your bills as quickly as possible.

ATM cards (Automated Teller Machine) are debit cards. They automatically withdraw money from your account.

Some consumers prefer to use debit cards rather than credit cards because debit cards don't incur interest charges.

PAYING OFF DEBT VS. SAVING – if you have credit card or other debt, it usually makes sense to pay off this debt first before contributing to savings. The interest rate you will get on savings is likely to be far less than the amount of credit interest you are paying.

ACT – IMPLEMENT YOUR PLAN/ASSESS/ADJUST

Once you have set goals, estimated your fixed and variable expenses and identified monthly savings targets, it is time to put your plan to work.

Give it some time. Then see how you are doing. Were you able to meet your savings goals? If so, stick with it. If not, look at your variable expenses for opportunity areas to cut back spending and increase savings.

Evaluate your plan every three months and make adjustments as needed. If you are not saving enough to meet your monthly goals, you may need to spend less.

Saving is the key to successful financial plans. Use payroll deductions or automatic transfers to checking, savings or money market accounts. It is easier to save if you never see the money.

Use budget plans for paying utilities if they are available. Use cash for purchases rather than charging if you can.

Enter each check you write in a check register. Balance the account every month. If you use a debit card, enter those amounts in your check register.

SELECT A FINANCIAL INSTITUTION

Creating a safety net is easier if you work with a good financial institution such as a credit union or bank.

Interview employees at several locations; look for people who are willing and able to answer your questions. Be ready to talk about the services and the advice you need.

For example, if it is important to you to conduct transactions face-to-face rather than by Automatic Teller Machines (ATM), ask if the financial institution charges for the services of a person at the counter. If you prefer to use ATMs, make sure they are readily accessible and do not charge transaction fees.

Once you select a financial institution, consider opening a checking account if you do not have one. A checking account can save you fees you may now be paying for cashing your paycheck and paying your bills.

START NOW AND STICK WITH IT. YOU WILL FIND THAT BEING SMART ABOUT MONEY IS WELL WORTH IT.

No comments:

Post a Comment